Established Business Equipment Finance Guide

An established business equipment finance guide for evaluating terms, preserving working capital, and putting revenue-producing assets into service now.

A vendor financing partnership program guide should start with the point where many equipment sales stall: the customer wants the truck, trailer, excavator, or forklift, but needs a workable capital plan before signing the purchase order. For established dealers and manufacturers, a financing partner can help turn a qualified buyer’s interest into a structured transaction without forcing the sales team to become credit analysts.

The right program does more than place an application. It supports the sales process, identifies financeable transactions early, coordinates documentation, and helps keep the equipment, borrower profile, and lender requirements aligned through funding. That matters when a delayed replacement truck, unfinanced wrecker, or unavailable construction machine puts a customer’s revenue plan on hold.

A vendor financing partnership program connects an equipment seller with a commercial equipment finance broker or financing partner that can evaluate buyer financing requests and source appropriate options through multiple funding sources. The vendor sells the asset. The financing partner works with the buyer and prospective funding source on credit, structure, required documents, and closing conditions.

For the vendor, the practical objective is simple: reduce avoidable friction between quote and delivery. For the buyer, the objective is to preserve working capital while putting revenue-producing equipment into service.

This arrangement can apply to new and used commercial assets, including semi-trucks, trailers, tow trucks, dump trucks, box trucks, car haulers, buses, ambulances, excavators, loaders, forklifts, and specialized industrial equipment. The equipment category matters because lenders often evaluate useful life, age, mileage, condition, title status, and resale market differently.

A late-model sleeper truck with documented mileage and a recognized VIN is not underwritten the same way as a 15-year-old specialty wrecker or a custom-built industrial unit. A capable financing partner helps identify those distinctions before the deal reaches the finish line.

Most commercial customers do not evaluate equipment on purchase price alone. They are weighing monthly payment, down payment, term length, delivery timing, expected utilization, maintenance exposure, and the cash required to operate the asset once it arrives.

A financing conversation gives the sales team a way to discuss the total acquisition plan rather than only the sticker price. A $180,000 rollback may be well within an established towing company’s operating plan if the payment, expected calls, insurance costs, and driver availability support the transaction. The same unit may not be a fit if the business is already stretched by recent expansion or cannot document sufficient cash flow.

A good vendor program can also help sales teams avoid spending weeks on transactions that are unlikely to fit standard lender parameters. This is not about pre-judging every customer. It is about asking sensible early questions: How long has the business operated? What equipment does it already own? Is this a replacement or an expansion? What is the asset’s age and mileage? Does the buyer have financial statements or recent bank statements available?

When those basics are addressed early, the vendor can set more realistic expectations around approvals, deposits, delivery dates, and document requirements.

A vendor program should be built around process, not vague promises of fast financing. The seller needs a clear handoff process, the buyer needs informed communication, and the financing partner needs accurate transaction details.

The finance request should include a detailed quote or buyer’s order that identifies the seller, buyer, purchase price, any trade allowance, serial number or VIN when available, equipment condition, year, make, model, mileage or hours, and expected delivery date. For titled commercial vehicles, title status and lien information can affect timing.

Used equipment requires particular care. A lender may have different guidelines for a 2022 tractor with 350,000 miles than for a 2016 tractor with 800,000 miles, even if both are priced similarly. The same is true for yellow iron with high operating hours or equipment modified for a specialized use.

Established businesses generally present a clearer financing picture when they can document time in business, ownership, credit strength, operating history, revenue, existing debt, and equipment use. Fleet size and prior payment history can also matter, especially for transportation and vocational operators.

The buyer should be prepared to explain whether the asset replaces an aging unit, adds capacity under contract, supports a new service line, or fills a seasonal need. Lenders often view a replacement that protects uptime differently from a speculative expansion, though either may be financeable depending on the full file.

The best programs make it clear who handles each question. The vendor should remain focused on the equipment, specifications, delivery, and sale documentation. The financing partner should manage the application, lender communication, credit-related documentation, and funding conditions. The buyer should receive direct, professional updates without being bounced between parties.

This separation protects the relationship. Salespeople should not be asked to interpret a lender stipulation or explain why a personal guaranty, bank statement, insurance binder, or corporate resolution may be needed.

Start by mapping the equipment you sell and the buyers you serve. A trailer dealer selling primarily new dry vans to established fleets will have a different financing mix than a dealer selling used wreckers, crane trucks, or specialized forestry equipment. Asset type influences likely term lengths, advance rates, appraisal needs, and documentation expectations.

Next, decide when financing enters the sales conversation. Waiting until the buyer has chosen a unit can work for straightforward transactions, but it may create delays on higher-value, used, or specialized assets. For those deals, a preliminary finance discussion before final equipment selection can help the buyer shop within a practical range.

Then establish a consistent handoff. The sales representative should provide the equipment quote and introduce the buyer to the financing contact while the deal is active. The financing partner should confirm the information needed, assess potential structures, and communicate only what can be supported by the borrower profile, asset, and funding source requirements.

Finally, track outcomes that matter to the vendor: finance applications received, approvals, funded deals, average time from complete file to decision, lost deals, and the reasons transactions did not move forward. This feedback improves inventory choices and sales qualification over time.

Commercial equipment financing is not one product. Depending on the transaction, a buyer may consider an equipment loan, finance lease, operating lease, or another structured arrangement. The appropriate option depends on the asset, its expected useful life, the buyer’s accounting and operational preferences, and lender availability.

A longer term may reduce the monthly payment, which can help a buyer protect operating cash. It can also increase total financing cost and may not be available for older or high-mileage equipment. A larger down payment can improve the lender’s collateral position and may broaden available options, but it uses cash that the buyer may need for insurance, payroll, fuel, repairs, or mobilization.

Low-down-payment or, in some cases, zero-down structures may be available for well-qualified businesses and suitable assets. They are never automatic. Credit profile, time in business, liquidity, fleet history, equipment age, seller type, and the requested structure all affect what a funding source may consider.

For vendors, the lesson is to avoid presenting a monthly payment as a promise before the financing file is reviewed. A responsible estimate can be useful, but final terms depend on the completed transaction.

Many funding delays are preventable. The most common issue is incomplete or inconsistent documentation. The equipment quote may show one price while the buyer’s order shows another. A VIN may be missing. A used unit may not have a clear ownership trail. The buyer may apply under an entity name that does not match its tax or banking records.

Insurance is another frequent closing item for titled vehicles and high-value equipment. The buyer may need coverage that meets the funding source’s requirements before documents can be released or funded. Delivery timing, title work, payoff letters on trade-ins, and inspection requirements can also affect the closing sequence.

A vendor should not treat these items as paperwork afterthoughts. They are part of the transaction plan. The earlier they are identified, the easier it is to protect the buyer’s delivery schedule.

A vendor should look for a financing partner that understands commercial equipment and can communicate clearly with both sales teams and established business buyers. Industry familiarity matters when the transaction involves mileage limits, used-asset valuations, vocational bodies, upfitting, seasonal revenue, or equipment that does not fit a generic credit box.

CFF works as a specialized commercial equipment finance broker and financing partner, coordinating qualified business transactions across multiple funding sources. That model can be useful when a vendor’s customers and inventory vary by asset age, industry, purchase size, and borrower profile.

Before formalizing a relationship, discuss the types of assets sold, typical transaction sizes, buyer profiles, documentation process, communication expectations, and how exceptions will be handled. A program that is efficient for new fleet trailers may need a different approach for used tow trucks or custom vocational builds.

The strongest vendor financing relationships are practical: the seller provides accurate equipment information, the buyer provides a complete business profile, and the financing partner structures the file around the real transaction. That gives qualified customers a clearer path from equipment quote to equipment in service, while helping vendors keep their sales process focused on what they know best.

An established business equipment finance guide for evaluating terms, preserving working capital, and putting revenue-producing assets into service now.

Choosing a commercial financing partner Texas businesses can rely on means weighing equipment knowledge, lender access, structure, and responsive execution.

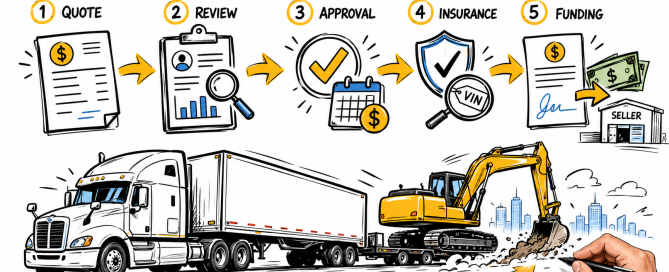

Understand the equipment finance process, from equipment quote and credit review through approval, documentation, vendor payment, and delivery planning.

A construction equipment loan review for established businesses: assess terms, collateral, cash flow, asset age, and lender fit before you fully commit.

Fleet financing helps businesses replace, expand, or upgrade revenue-producing equipment while managing cash flow, uptime, and lender requirements well.