Established Business Equipment Finance Guide

An established business equipment finance guide for evaluating terms, preserving working capital, and putting revenue-producing assets into service now.

A trailer that fits your route, freight, and timeline can start producing revenue quickly. The financing side is where many buyers slow down. With new vs used trailer financing, the better choice is not always the cheaper unit or the newer spec – it is the structure that best supports cash flow, uptime, and the useful life of the asset.

For a fleet adding dry vans, a contractor buying equipment trailers, or an owner-operator replacing an aging reefer, the decision usually comes down to more than purchase price. Age, condition, down payment, documentation, approval profile, and how long you plan to run the trailer all matter. A smart financing decision should line up with the way the trailer will earn money.

At a high level, new trailers tend to be easier to finance on longer terms because they offer more remaining useful life and fewer condition concerns. Used trailers can still be financeable, often very effectively, but the deal structure may be tighter depending on the trailer’s age, mileage if applicable, maintenance history, and intended use.

That difference matters because lenders look at collateral risk and repayment risk together. A newer trailer may support a lower down payment or longer amortization in some cases because the asset is easier to value and often expected to stay in service longer. A used trailer may still be the better business move if the purchase price is lower and the trailer can be put to work right away without major reconditioning.

In other words, the question is not whether new is better than used. The real question is whether the financing terms and total cost make sense for your operation.

New trailer financing often appeals to buyers who want predictability. If you are ordering multiple units for fleet growth, standardizing trailer specs, or replacing old equipment with minimal downtime, a new trailer can simplify operations. Maintenance is usually easier to forecast, and the asset may stay in service long enough to justify a longer payment term.

That can help with monthly cash flow. Even if the purchase price is higher, spreading the cost over a longer period can make the payment manageable, depending on the borrower profile and lender program. For businesses focused on uptime, warranty coverage and reduced repair risk can offset the higher upfront cost.

New equipment can also help in customer-facing operations where appearance, reliability, and compliance matter. Think medical transport support trailers, enclosed specialty trailers, car haulers, or trailers tied to time-sensitive freight. If a breakdown costs you revenue or customer confidence, the added cost of new may be justified.

The trade-off is obvious. You are financing a higher principal amount. That may increase total dollars paid over time, even if the monthly payment looks workable. Buyers should weigh the financing structure against actual utilization. If the trailer will not be heavily used, paying a premium for new may not produce a strong return.

Used trailer financing often works well for businesses that know exactly what they need and want to preserve capital. A well-maintained used flatbed, dump trailer, dry van, or utility trailer can generate revenue without the price tag of a factory-new unit.

For many commercial buyers, that lower acquisition cost is the main advantage. It may reduce the amount financed, lower the down payment requirement in dollar terms, and shorten the path to positive cash flow. If you are adding capacity for a new contract, seasonal demand, or a secondary route, used equipment can be the practical choice.

Used can also be the right answer when the equipment market is tight. If lead times on new trailers are long, waiting may cost more than buying a solid used unit today. In revenue-producing equipment finance, timing matters. A trailer in service now is often more valuable than a perfect spec months from now.

The catch is that used trailer financing can become more document-driven. Lenders may want more detail on the trailer’s condition, age, VIN, maintenance records, purchase source, and valuation support. Older units can face shorter terms or additional scrutiny. That does not mean the deal cannot get done. It means the structure has to fit the asset.

Whether you are comparing new vs used trailer financing for one unit or an entire fleet, lenders are generally evaluating the same core issues.

First is the borrower. Time in business, credit profile, revenue, industry, and overall repayment strength all influence available options. A strong borrower may have more flexibility on structure, even with used equipment. A newer business may still qualify, but the file may need more support or a different down payment approach.

Second is the trailer itself. Type, age, condition, manufacturer, and expected useful life all matter. A late-model trailer from a recognized manufacturer with clean documentation is usually easier to place than an older unit with unclear history or visible wear.

Third is the transaction. Where the trailer is being purchased, how it is priced, whether the valuation makes sense, and how quickly documents can be gathered all affect the process. Dealer transactions are often more straightforward than private-party transactions, though both may be possible depending on the deal.

Many buyers focus on payment first, and that is understandable. But a lower payment does not automatically mean a better financing outcome.

If a used trailer has a low purchase price but needs brakes, tires, floor work, refrigeration service, or structural repairs within the first six months, the real cost can change fast. On the other hand, financing a new trailer at a higher amount may protect cash flow if it reduces repair exposure and keeps the unit moving consistently.

This is where total operating cost matters. Look at the full picture: down payment, monthly payment, likely repair spend, downtime risk, and how much revenue the trailer should generate during the finance term. A cheap trailer that sits in the yard waiting for repairs is not cheap.

Trailer buyers often need equipment on a deadline. A freight contract starts next week. A customer needs more capacity. A damaged trailer has to be replaced. In those situations, financing efficiency matters almost as much as the rate or term.

New trailer deals can sometimes move faster because the equipment specs, invoice, and seller documentation are cleaner. Used deals can also move quickly, but they may require more back-and-forth if the asset is older or the records are incomplete. Missing VIN details, inconsistent bill-of-sale terms, or limited condition information can slow the process.

That is why it helps to work with a commercial financing partner that understands trailer categories, lender requirements, and how to present the file correctly. A well-structured file can make a meaningful difference in approvals, terms, and funding timelines.

If your operation depends on high utilization, customer-facing reliability, or fleet standardization, new often deserves a close look. The same is true if you want longer useful life and fewer near-term maintenance variables.

If your priority is conserving capital, covering a shorter-term need, expanding capacity at a lower cost, or buying proven equipment with a known service history, used may be the stronger move.

There is also a middle ground that makes sense for many businesses: late-model used trailers. These units can offer better value than new while still fitting within acceptable age and condition ranges for competitive commercial financing structures.

The best financing choice supports the trailer’s job in your business. A dump trailer for daily production work, a reefer for temperature-sensitive loads, and a flatbed for occasional overflow capacity should not all be financed the same way. Asset use, urgency, trailer age, and borrower profile should drive the structure.

For many businesses, the smartest move is to evaluate the trailer and the financing together, not separately. A lower purchase price is only useful if the equipment stays productive. A newer trailer is only worth the premium if the added cost improves uptime, resale position, or operating efficiency.

Commercial Fleet Financing works with businesses across the U.S. to finance revenue-producing trailers and equipment based on real operating needs, asset details, and deal structure. If you are weighing new against used, the goal is simple: match the financing to the work the trailer needs to do, then keep your business moving.

An established business equipment finance guide for evaluating terms, preserving working capital, and putting revenue-producing assets into service now.

Choosing a commercial financing partner Texas businesses can rely on means weighing equipment knowledge, lender access, structure, and responsive execution.

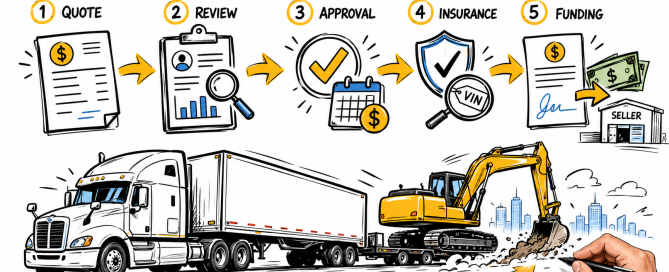

Understand the equipment finance process, from equipment quote and credit review through approval, documentation, vendor payment, and delivery planning.

A construction equipment loan review for established businesses: assess terms, collateral, cash flow, asset age, and lender fit before you fully commit.

Fleet financing helps businesses replace, expand, or upgrade revenue-producing equipment while managing cash flow, uptime, and lender requirements well.