Established Business Equipment Finance Guide

An established business equipment finance guide for evaluating terms, preserving working capital, and putting revenue-producing assets into service now.

A machine sitting in the yard does not produce revenue. A machine on the jobsite can help a contractor finish work, take on the next project, and avoid the cost of repeated repairs on aging iron. That is the business case behind how to finance construction equipment: matching the payment structure, equipment life, and approval file to the work the asset will perform.

For established contractors, demolition companies, landscapers, utility crews, and other equipment-dependent businesses, the lowest monthly payment is not always the best answer. The right structure has to preserve working capital while keeping the machine available, reliable, and suited to the contracts ahead.

Before requesting financing, define what the equipment will do and how quickly it should generate billable work. A compact track loader for a landscaping company, an excavator for a sitework contractor, and a dozer for a heavy civil operation may all be financed assets, but they carry different utilization patterns, maintenance needs, and resale considerations.

Ask whether the purchase is a replacement, an expansion, or a specialized addition to the fleet. A replacement may reduce downtime and repair expense. An additional machine may be tied to a signed contract, a larger backlog, or the ability to self-perform work that was previously subcontracted. Those distinctions help explain the transaction to a financing source and help the buyer decide how much payment the business can reasonably support.

The equipment itself matters as well. New machines from established manufacturers are often easier to place than older, highly specialized, or unusually configured equipment. Used equipment can be a sound purchase, particularly when it has service records and comes from a reputable dealer, but age, hours, condition, and expected remaining useful life can affect available term length, advance rate, and down payment requirements.

Construction equipment financing is commonly structured as an equipment loan or as a lease. The practical difference is not just terminology. It affects ownership, payment design, end-of-term options, and how the transaction fits the company’s financial plan.

With an equipment loan, the business generally owns the machine after the loan is paid off, subject to the lender’s security interest during the term. This approach often fits companies that expect to keep an excavator, skid steer, loader, or other asset for a long service life.

A loan may make sense when the buyer wants a predictable path to ownership and expects the equipment to retain useful value after the financing term. The trade-off is that the payment structure must fit the machine’s age and collateral value. Stretching payments too far on an older unit can create challenges if its condition declines faster than expected.

An equipment lease can offer different end-of-term arrangements, depending on the program. Some structures are designed for ownership, while others provide an option to return, renew, or purchase the equipment at the end of the term. This can be useful when a business wants to manage replacement cycles, preserve flexibility, or align the financing period with expected use.

A lease is not automatically better because the payment is lower. A lower payment may reflect a residual or purchase option due at the end. Review that obligation, along with any mileage or usage limitations where applicable, before comparing proposals.

Qualified established businesses may have low-down-payment or, in some cases, zero-down options available. Those outcomes depend on credit strength, time in business, existing fleet and equipment history, the asset, seller, documentation, and the overall deal structure. A larger down payment can reduce the monthly obligation and may improve the financeability of older equipment, but it also takes cash away from payroll, materials, fuel, insurance, and mobilization.

Term length should reflect the equipment’s remaining useful life, not simply the longest payment available. A 60-month structure may work well for a newer, broadly marketable machine. A shorter term may be more realistic for an older excavator with high hours or a niche attachment with limited resale demand.

Strong businesses can still lose time when the equipment file is incomplete. The goal is to give the financing source a clear picture of the borrower, the collateral, and the business purpose without creating unnecessary back-and-forth.

For many commercial equipment transactions, expect to provide a formal quote or purchase order showing the seller, equipment description, serial number when available, purchase price, and any attachments. For used equipment, year, hours, condition details, and photographs may matter. A dealer sale is generally more straightforward than a private-party purchase, although private sales can be financeable when ownership, payoff, and equipment condition are properly documented.

The borrower file may include business formation information, tax identification details, recent business bank statements, financial statements, tax returns, debt schedules, and ownership information. The exact request varies by transaction size, credit profile, and lender requirements. A well-established company with strong commercial credit and a documented operating history may receive a more streamlined review than a transaction involving an older asset, a higher leverage position, or a complex ownership structure.

Be prepared to explain the intended use. “General construction” is less helpful than “replacing a 2014 excavator with recurring hydraulic repairs for a utility trenching fleet operating under current municipal and commercial contracts.” Specificity shows the asset supports a real operating need.

When comparing financing proposals, look beyond the monthly number. A payment can appear attractive because the term is longer, the final purchase option is larger, or required fees have been handled differently. Compare the amount financed, payment frequency, term, any advance payment or down payment, end-of-term obligation, documentation fees, and prepayment provisions.

Payment timing also matters in construction. A company with uneven project billing may prefer a structure that aligns with its cash conversion cycle, provided the financing source supports it. Seasonal payment designs may be possible in certain situations, but they are not universal and require a lender willing to structure around the business’s documented operations.

Consider the ownership cost after closing. Insurance, transport, attachments, maintenance, operator training, and the working capital needed to put the machine into service all belong in the acquisition plan. Financing the base machine while overlooking a costly bucket package, trailer, or required technology can leave a purchase undercapitalized.

Commercial equipment financing decisions are based on both the business and the machine. Credit strength matters, but it is only part of the file. Financing sources commonly consider time in business, annual revenue, profitability, existing debt, payment history, fleet size, prior equipment ownership, and the concentration of work among a few customers.

They also evaluate the collateral. A late-model, standard excavator from a recognized manufacturer with reasonable hours is different from a high-hour specialty machine, a rebuilt unit, or equipment purchased without a verifiable serial number. Seller type matters because dealers, manufacturers, auctions, and private sellers each create different documentation and funding considerations.

A contractor with good credit may still be asked for additional information if the equipment cost is large relative to revenue or if several units are being added at once. Conversely, a business with a strong operating history, clear financials, and a replacement purchase may have a more straightforward path. There is no responsible way to promise an approval, rate, or funding date before the full transaction is reviewed.

A specialized equipment finance broker can help an established business present the transaction to appropriate funding sources and compare structures without treating every machine like a standard vehicle loan. This is particularly valuable when the purchase includes used yellow iron, multiple units, attachments, private-party equipment, or a time-sensitive dealer delivery.

Commercial Fleet Financing, Inc. works with qualified businesses nationwide on commercial equipment transactions and can help coordinate the borrower file, vendor documents, and financing process. Approval and funding speed can vary materially based on the credit profile, asset, seller, documentation, lender requirements, and transaction structure, but early preparation reduces avoidable delays.

The most productive next step is to gather the equipment quote, a brief description of its intended work, and current business financial information before committing to a purchase. That gives your team a clearer basis to evaluate the payment, the term, and whether the machine will strengthen operations rather than strain cash flow.

An established business equipment finance guide for evaluating terms, preserving working capital, and putting revenue-producing assets into service now.

Choosing a commercial financing partner Texas businesses can rely on means weighing equipment knowledge, lender access, structure, and responsive execution.

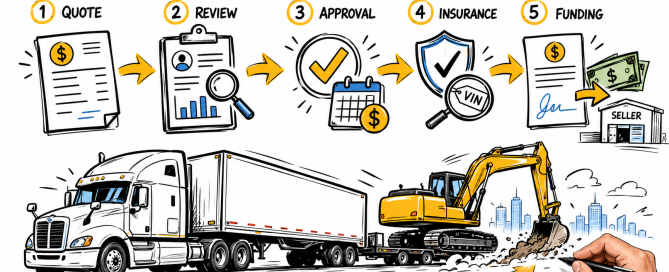

Understand the equipment finance process, from equipment quote and credit review through approval, documentation, vendor payment, and delivery planning.

A construction equipment loan review for established businesses: assess terms, collateral, cash flow, asset age, and lender fit before you fully commit.

Fleet financing helps businesses replace, expand, or upgrade revenue-producing equipment while managing cash flow, uptime, and lender requirements well.