Established Business Equipment Finance Guide

An established business equipment finance guide for evaluating terms, preserving working capital, and putting revenue-producing assets into service now.

A diesel replacement can usually be evaluated from the truck, its application, and the payment. Commercial electric vehicle financing trends add a fourth decision that cannot be separated from the asset: the charging plan. For an established fleet, the question is not simply whether an electric vehicle is available. It is whether the vehicle, route, charging capacity, operating cost, and financing structure work together well enough to keep revenue moving.

That is changing how borrowers, vendors, and financing sources evaluate electric box trucks, delivery vans, buses, vocational units, and other commercial EVs. A well-documented electric vehicle transaction can be financeable. But it generally requires more operational detail than a comparable conventional vehicle purchase.

A commercial vehicle is financed because it has a business use and is expected to generate revenue or support revenue-producing operations. With an electric vehicle, lenders and financing partners also need confidence that the business can put the unit into service as planned.

For a local delivery fleet, that may mean documented daily mileage, predictable return-to-base operations, and overnight depot charging. For a shuttle or medical transport operator, it may mean route timing, passenger loads, charging windows, and backup-vehicle availability. A construction or utility fleet may need to address power access at the yard, jobsite charging limitations, and the effect of auxiliary equipment on range.

These details do not make an EV transaction unworkable. They help determine whether the asset fits the business and whether the proposed payment aligns with expected utilization. A vehicle that runs a consistent 75-mile urban route is a different financing discussion from a truck expected to cover variable long-haul routes with irregular dwell time.

The purchase price remains central, but total project cost is becoming more relevant. Many commercial EV deployments involve equipment beyond the vehicle itself, including charging stations, electrical upgrades, installation work, software, and in some cases onsite energy equipment.

A borrower may prefer to finance the vehicle separately from charging infrastructure because the assets have different useful lives, collateral characteristics, vendors, and installation timelines. The vehicle may be titled and delivered quickly, while a charger installation depends on permits, utility coordination, site work, and electrical capacity. Separating the transactions can make documentation cleaner and prevent an equipment delivery from being held up by a delayed infrastructure project.

In other situations, combining eligible hard costs into one project may better match the fleet’s cash flow plan. It depends on the funding source, the asset mix, the vendor invoices, and whether the infrastructure is owned by the borrower. Soft costs, deposits, utility charges, and service agreements may be treated differently from vehicles and installed equipment.

The practical lesson is to build the financing request from a complete project budget, then identify what should be financed together and what should stand alone. A quote for the vehicle alone is often not enough for a meaningful capital-planning decision.

With a conventional used truck, underwriting often focuses on age, mileage, engine condition, maintenance records, and resale value. Those factors still matter for electric units, but battery health and remaining warranty coverage add another layer.

A newer EV with a manufacturer-backed battery warranty, known service history, and a clear commercial application is usually easier to evaluate than an older unit with uncertain charging history or limited support. Financing sources may also look closely at the availability of qualified service, replacement parts, and a secondary market for the specific model.

This is especially relevant for used electric vans and trucks. A lower acquisition cost can improve the payment, but it may also bring a shorter remaining battery warranty, older charging hardware, or less predictable residual value. Fleet managers should request available battery-health information, warranty documents, maintenance history, and confirmation that the vehicle’s charging connector and power requirements fit the planned site.

There is no universal maximum age or mileage threshold for commercial EV financing. Asset eligibility varies by lender, vehicle type, manufacturer, borrower strength, and term length. Still, the more unusual or aged the asset, the more the financing structure may need to compensate through a larger down payment, shorter term, or additional documentation.

Residual value is the expected value of an asset at the end of a lease or financing term. It matters because commercial EV technology, battery performance, model availability, and used-market demand are still developing across many vehicle classes.

That uncertainty does not automatically mean a borrower should avoid leasing or insist on a short term. It means the structure should match the fleet’s replacement strategy. A business that expects to operate a vehicle for many years may value a financing structure that supports ownership at the end of term. A fleet that wants flexibility as technology develops may place more value on an end-of-term option, provided it understands the mileage limits, condition requirements, and return obligations.

Common structures can include an equipment finance agreement or loan, a finance lease with a fixed end-of-term purchase option, and a fair market value lease. Each handles ownership and end-of-term value differently. The best fit depends on expected annual miles, service life, maintenance responsibilities, accounting preferences, and how confident the fleet is in the asset’s long-term role.

The lowest monthly payment is not always the lowest-cost or lowest-risk choice. A structure with a lower payment may rely on an end-of-term residual assumption that deserves careful review. Conversely, a higher payment that builds equity may make sense for a vehicle the business intends to retain well beyond the contract term.

Strong business credit, time in business, and a stable operating history remain important. For EV transactions, the charging plan increasingly helps complete the underwriting picture.

A useful file explains where the vehicle will charge, who controls the site, whether the business owns or leases the property, the expected charging schedule, and whether the electrical work is underway or complete. If the fleet relies on public charging, it should show why that approach is practical for the route and operating schedule.

For example, an established last-mile operator adding four electric step vans may present route records showing each unit returns to the same facility every evening. It may also provide a charger quote, a site plan, and evidence of adequate electrical capacity. That is materially different from stating that charging will be arranged after delivery.

Borrowers do not need to turn a finance application into an engineering report. They do need a credible deployment plan. Clear information can reduce avoidable questions after credit approval, when vendor documents, insurance requirements, delivery timing, and funding conditions are being coordinated.

Electric vehicle decisions are often framed around fuel and maintenance savings. Those may be meaningful, but a commercial fleet should also examine uptime and operational resilience.

If an electric vehicle eliminates frequent fueling stops and works reliably within a fixed route, it may support a favorable operating case. If a charger outage, insufficient site power, or route deviation creates service disruptions, the savings estimate may not tell the whole story. Backup units, charger maintenance agreements, driver training, and dispatch procedures all affect the real economics.

This is why financing terms should be considered alongside the expected ramp-up period. A fleet may want to preserve working capital while it trains drivers and validates routes. Another business may choose a larger down payment to reduce fixed monthly obligations during an initial deployment. Neither approach is automatically better. The right decision depends on cash reserves, utilization, contract revenue, seasonality, and the fleet’s tolerance for new-technology risk.

A complete financing package helps a specialized financing partner match the transaction to appropriate funding sources. For an electric commercial vehicle purchase, the core items usually include the vehicle quote or buyer’s order, detailed equipment specifications, business financial information requested by the financing source, and recent bank statements when required.

It is also useful to have the business’s time in operation, fleet size, existing equipment schedule, intended use, annual mileage estimate, delivery date, seller information, and charging plan ready. If the transaction includes chargers or electrical work, separate quotes and a clear ownership explanation can prevent confusion about what is being financed.

Established borrowers with strong credit and documented fleet history may have more structure options. Even then, terms can depend on the vehicle manufacturer, asset age, down payment, requested term, financial profile, seller type, and lender-specific requirements. A clean, complete file is often more valuable than trying to force a one-size-fits-all structure.

Commercial EV adoption is becoming less about making a broad technology statement and more about matching the right asset to the right route. The financing conversation should follow the same discipline.

Commercial Fleet Financing, Inc. works as a specialized equipment finance broker and financing partner, helping qualified established businesses present vehicle and equipment transactions to multiple potential funding sources. The most productive first discussion covers the unit being acquired, its work cycle, the charging plan, the vendor timeline, and the cash flow the business needs to protect. When those pieces are clear, financing can support a measured fleet upgrade rather than create another operational variable to manage.

An established business equipment finance guide for evaluating terms, preserving working capital, and putting revenue-producing assets into service now.

Choosing a commercial financing partner Texas businesses can rely on means weighing equipment knowledge, lender access, structure, and responsive execution.

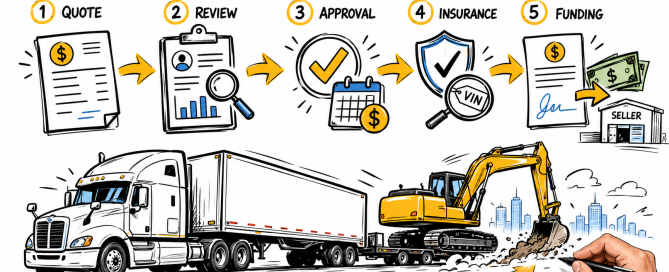

Understand the equipment finance process, from equipment quote and credit review through approval, documentation, vendor payment, and delivery planning.

A construction equipment loan review for established businesses: assess terms, collateral, cash flow, asset age, and lender fit before you fully commit.

Fleet financing helps businesses replace, expand, or upgrade revenue-producing equipment while managing cash flow, uptime, and lender requirements well.