Established Business Equipment Finance Guide

An established business equipment finance guide for evaluating terms, preserving working capital, and putting revenue-producing assets into service now.

A bus that is waiting on financing is not carrying passengers, fulfilling a contract, or producing revenue. For established fleets, commercial bus financing for operators is less about finding a generic payment and more about matching the transaction to the bus, route economics, operating history, and timing of the replacement or expansion.

A late-model motorcoach headed into charter service presents a different financing profile than a used cutaway bus for non-emergency medical transportation or a shuttle bus serving an airport contract. The asset, seller, mileage, intended use, and business documentation can all affect lender appetite and the structure available. Addressing those details before a purchase order is signed can prevent delays when the bus needs to enter service.

The payment matters, but it should not be the first decision. Start with what the bus is expected to do: replace an unreliable unit, add capacity under an existing contract, enter a new service line, or meet a customer or regulatory requirement. That purpose helps determine an appropriate term, down payment, and equipment choice.

For example, a fleet replacing a high-mileage shuttle bus may prioritize reliability and maintenance savings. A longer repayment term might preserve working capital, but it should still make sense relative to the bus’s expected useful life and condition. A company adding buses for a documented municipal, university, hotel, or charter opportunity may instead focus on getting appropriately configured equipment into service by a firm start date.

The lowest payment is not automatically the best outcome. Extending a term can improve near-term cash flow, but it may increase total financing cost and leave a balance outstanding longer. A larger down payment can strengthen a transaction and reduce the payment, yet it also ties up cash that may be needed for insurance, licensing, payroll, maintenance reserves, or initial operating expenses.

Commercial bus transactions are generally evaluated as both a borrower and an asset decision. Established companies with documented operating history, good to strong business and personal credit profiles, and a record of managing commercial equipment are often in a better position than businesses attempting to finance outside their demonstrated operating model.

Lenders commonly look at time in business, ownership structure, business and personal credit, bank activity, revenue trends, existing debt, and payment history. They also want to understand how the new bus fits the operation. A transportation company adding a similar unit to an established fleet is easier to explain than a company purchasing a specialized passenger vehicle with no related operating history.

Fleet experience carries weight. A borrower operating several buses, maintaining commercial insurance, and showing consistent passenger-service revenue can present a clearer story than a company with no comparable assets. That does not mean every expansion requires years of bus ownership, but the operating plan and supporting records become more important when the equipment represents a new category or a material increase in fleet size.

Bus type, age, mileage, condition, make, model, seating configuration, accessibility equipment, and expected resale value can affect financing options. New equipment from an established dealer is often simpler to document than an older bus sold privately. Used buses can be financeable, but lenders may place more emphasis on age, mileage, maintenance records, inspection history, and valuation.

A high-mileage coach may be perfectly usable for a certain route, yet it may not fit every lender’s collateral guidelines or preferred term. Similarly, a bus with extensive conversion work, unusual branding, or highly specialized passenger configuration may require closer review. The right question is not whether used equipment is “good” or “bad.” It is whether its condition, value, and remaining service life support the requested structure.

A complete file reduces avoidable back-and-forth. Depending on the deal, requested items may include a vendor quote or purchase order, equipment specifications, vehicle identification number, photos, maintenance records, recent business bank statements, financial statements, tax returns, debt schedule, proof of insurance, and entity documents.

The seller matters as well. A recognized dealer generally provides standardized invoices, title documentation, and payoff information when applicable. Private-party purchases can require additional verification of ownership, liens, condition, and funds flow. If a bus is being purchased from an out-of-state seller, title and registration timing should be considered early rather than treated as an afterthought.

A commercial equipment loan or finance agreement typically provides a defined repayment schedule and is often used when the business intends to retain the bus long term. A lease structure may be considered when the company wants a different payment profile, end-of-term option, or equipment refresh strategy. The appropriate structure depends on lender programs, the asset, the business profile, and the company’s accounting and operating preferences.

Rather than treating loan versus lease as a universal choice, evaluate the practical tradeoffs. A bus used heavily in daily route service may be kept well beyond its repayment term if maintenance history and utilization support it. A charter fleet that refreshes equipment on a more deliberate cycle may value a structure that aligns with replacement planning. Accounting and tax treatment should be reviewed with the business’s own tax and accounting advisors, not assumed from a financing quote.

Down payment is another variable, not a fixed rule. Well-qualified established operators may have access to lower-down-payment structures in some situations, while older equipment, higher leverage, limited liquidity, or a more complex transaction can call for more equity. The strength of the borrower, condition of the bus, and requested term all interact.

Operators often find the right bus first and seek financing after committing to a delivery date. That can work when the documentation is straightforward, but it creates risk when the equipment is used, the seller is private, or the unit must be inspected, titled, converted, or insured before deployment.

Before placing a nonrefundable deposit, confirm the basic deal facts: exact vehicle details, seller identity, purchase price, delivery expectations, title status, and whether there is an existing lien to be paid off. Ask what documentation is available and whether the quoted price includes conversion work, delivery, or other items that may need separate treatment.

For buses intended for passenger transportation, insurance deserves early attention. Coverage requirements, garaging location, passenger capacity, service type, and driver qualifications may affect how quickly a policy can be bound. Financing approval alone does not put a bus into service if insurance, registration, inspections, or customer-required specifications remain unresolved.

A commercial equipment finance broker can help organize the transaction before it reaches a funding source. That includes reviewing the borrower profile, matching the bus and use case to likely program parameters, identifying documentation gaps, and coordinating with the dealer or seller. It is especially useful when asset age, mileage, private-party purchase details, or a time-sensitive delivery schedule need careful attention.

Commercial Fleet Financing, Inc. works as a specialized financing partner for established businesses, with access to multiple funding sources rather than a single lending program. That can matter when a transaction needs a structure aligned with the fleet’s credit strength, equipment profile, cash-flow needs, and operating plan. Approval timing, terms, down payment, and funding speed remain conditional on the complete file, lender requirements, asset, and transaction structure.

The most productive next step is to assemble the bus quote and a clear picture of the operation before shopping only for a payment. A lender or financing partner can evaluate a well-defined business need far more effectively than a vehicle purchase with unanswered questions.

An established business equipment finance guide for evaluating terms, preserving working capital, and putting revenue-producing assets into service now.

Choosing a commercial financing partner Texas businesses can rely on means weighing equipment knowledge, lender access, structure, and responsive execution.

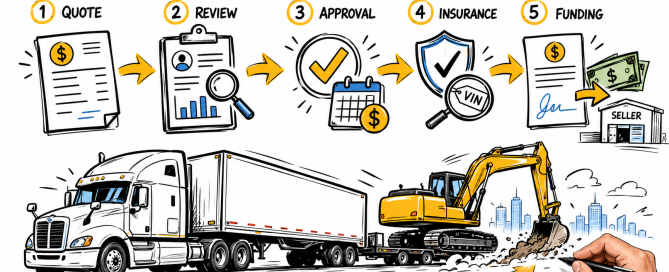

Understand the equipment finance process, from equipment quote and credit review through approval, documentation, vendor payment, and delivery planning.

A construction equipment loan review for established businesses: assess terms, collateral, cash flow, asset age, and lender fit before you fully commit.

Fleet financing helps businesses replace, expand, or upgrade revenue-producing equipment while managing cash flow, uptime, and lender requirements well.